x

Andrew LaSalla

Andrew LaSalla II is one of the most trusted financial consultants in the residential and commercial lending business. With over seven years of of property loan underwriting experience, Andrew's sole focus is helping clients successfully navigate complex financial laws, terms, rules, paperwork, and transactions necessary to secure loans for new construction, purchase, or refinancing of multifamily, healthcare, affordable housing and student housing properties. Whether it's HUD, FHA, or MAP loans, Andrew is committed to tailoring financial solutions for every client he serves.

By combining Low Income Housing Tax Credits (LIHTC) with 221(d)(4) HUD FHA financing, developers can raise capital to finance their project’s developments by partnering with investors. Ultimately, this means developers who typically construct apartments for market rates instead offer reduced market rents to meet the much-needed demand of affordable housing units throughout the U.S.

The Benefits of Combining LIHTC and HUD FHA Financing

The benefits of a HUD 221 (d)(4) transaction with LIHTC for affordable properties are:

- Reducing the Processing Time (Often Times Several Months)

- Reduced MIP Rates

- Reduced HUD Fees

- Higher Loan-To-Value Limits

Under the Land Use Restriction Agreement (LURA), developers who apply for LIHTC must meet low-income property requirements for the initial 15-year compliance period. LIHTC projects built after 1990 are required to remain affordable for an additional 15-years (for a total of at least 30 years), and some states require additional years.

How the LIHTC Works

Based on the state’s population, in 2018 the IRS allocated $2.40/person to each state’s housing authorities. States with minimal populations, e.g., Delaware or Alaska, receive at least $2,765,000. Developers must agree to one of these two options:

- >40% of the building’s units for tenants who earn <60% of the area’s median income OR

- >20% of the building’s units for tenants who earn <50% of the area’s median income.

The area’s median income limits are calculated using the county and metropolitan data from the U.S. Census Bureau’s American Community Survey. When developers are applying for the LIHTC, they must choose between:

- 9% LIHTC, which raises ~70% of the cost of the development (primarily used for new construction) OR

- 4% LIHTC, which raises ~30% of the cost of the development (primarily used to purchase an existing project and frequently combined with state bond financing).

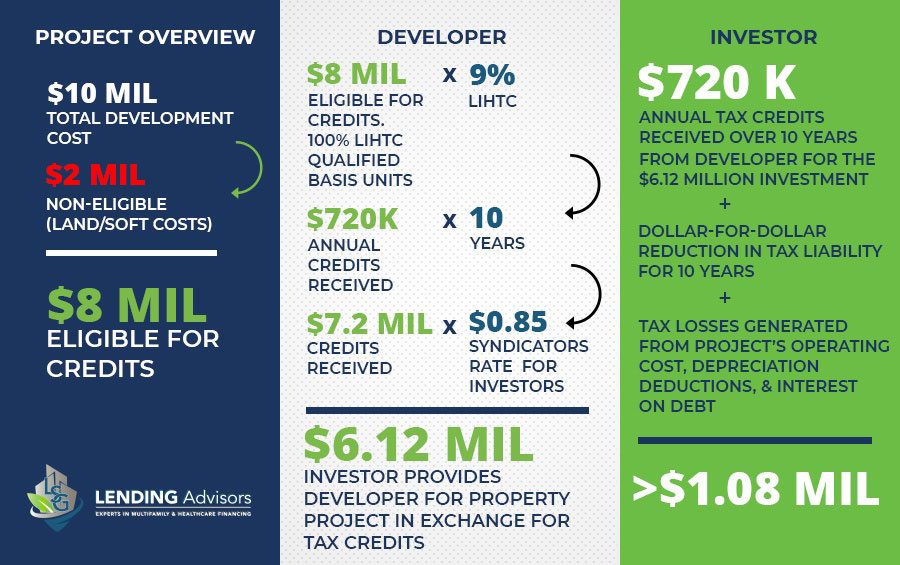

After making their decisions, developers apply to the state housing authority. Once the developers are approved for a certain amount of tax credits, the developers may choose to sell those tax credits to a syndicator for capital to fund the project’s construction costs. The syndicators then make those tax credits available to investors who purchase them for anywhere from $0.80-$0.95 on the dollar. The depreciation and interest expenses are then deducted from the investors’ taxable income.

Once construction, certificate of occupancy, and leasing agreements are completed per the agreement, the developer submits form 8608 along with the construction certificates, permits, and loan documents to receive the tax credits.

The Optimal Business Structure for Developers and Investors

Most developers and investors choose to create a Limited Partnership (LP) or Limited Liability Company (LLC). The developer is the General Partner who keeps a small percentage (usually 1%) with control of the day-to-day operations and manages the project. The investor is the Limited Partner who holds 99% ownership. The investor is allowed to claim an annual tax credit over a 10-year period. Typically, once these benefits end, the investor leaves the partnership.